The July Non-Farm Payrolls (NFP) report could offer much-needed clarity after a stronger-than-expected Q2 GDP print surprised markets. Although GDP grew at a 3.0% annualized rate, much of that gain came from falling imports and inventory drawdowns—not from rising consumer or business demand.

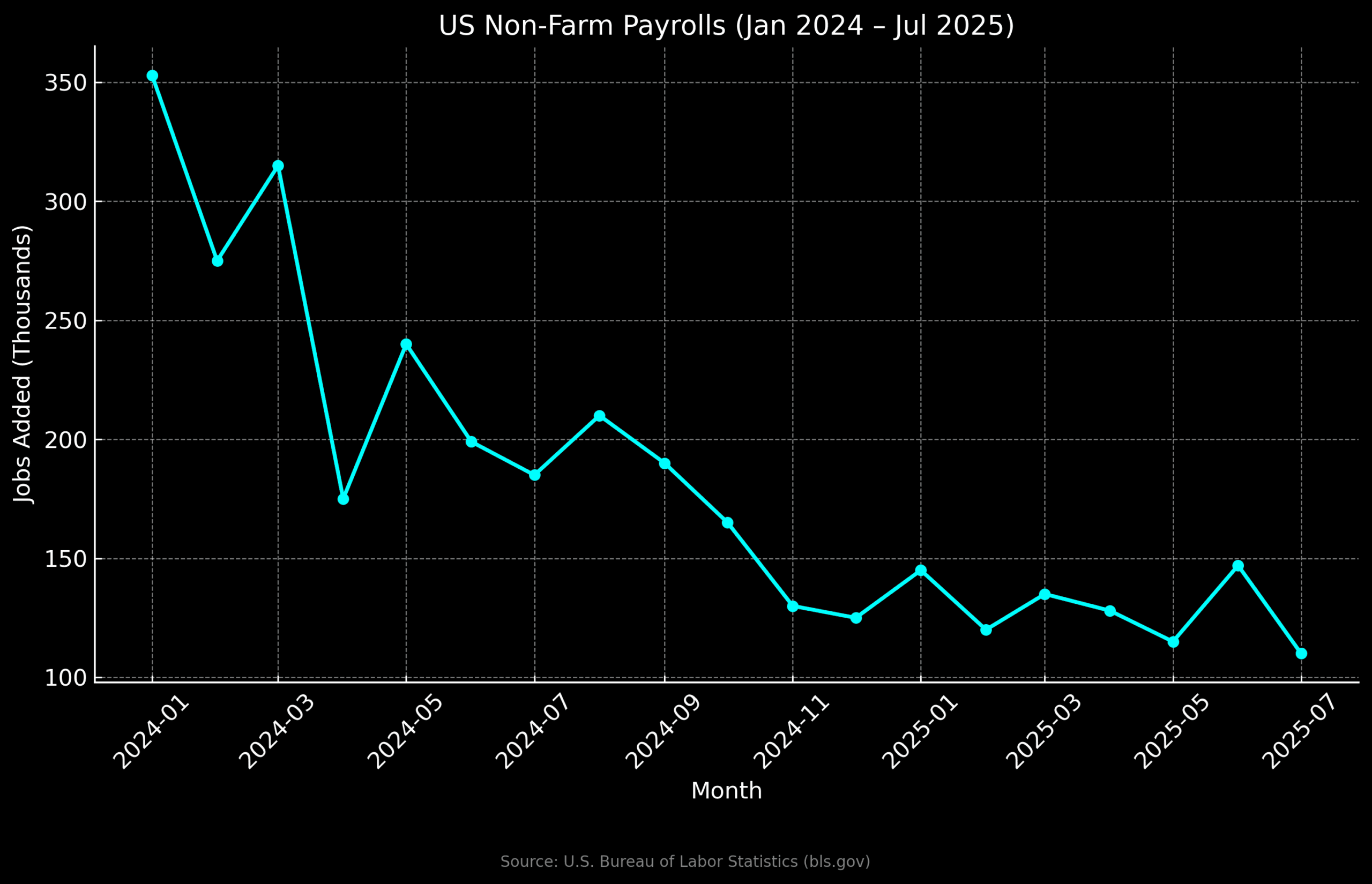

With forecasts pointing to a 110,000 job increase in July, down from 147,000 in June, the labour market appears to be slowing. Some analysts expect an even lower figure, around 95,000, due to weaker public sector hiring. This would align with the Federal Reserve’s goal of cooling demand without triggering a sharp rise in unemployment.

Unemployment is projected to tick up to 4.2%. Average hourly earnings are expected to grow at an annual pace of 3.9%. Wage growth remains a key metric. Stronger gains could renew inflation fears. Slower wage increases would support the Fed’s case for patience or even a policy shift.

Structural pressures—like aging demographics and lower immigration—limit how much the labour force can expand. These constraints may continue to push wages higher even if job creation slows. That could make it harder for the Fed to ease policy without risking inflationary rebound.

If Friday’s NFP report disappoints, the Fed may face more pressure to cut rates earlier than currently expected. Conversely, a stronger-than-forecast report—above 150,000 jobs—would point to lingering strength in the job market. That could push rate cuts further out and support both the U.S. dollar and Treasury yields. You can track the official figures via the Bureau of Labor Statistics.

Stocks remain strong, with the S&P 500 and Nasdaq 100 climbing to new highs. However, RSI on the S&P 500 shows a potential bearish divergence. The RSI has not confirmed recent price highs. If it fails to break above 76.75, a near-term pullback could follow.

The July NFP will act as a stress test for market sentiment. It may either reinforce the strength implied by headline GDP or expose the fragility beneath the surface. Either way, it’s likely to move both markets and monetary policy expectations.