AUD/USD pressured by RBA outlook and US jobs data remains a key market theme as traders weigh upcoming central bank moves. The Australian dollar slipped after recent inflation figures pointed to cooling prices, while mixed US signals added uncertainty.

Australia’s second-quarter inflation showed signs of easing. The RBA’s preferred measure, the trimmed mean CPI, rose just 0.6% quarter-on-quarter. The annual rate dropped to 2.7%, pulling inflation closer to the central bank’s 2–3% target range. When combined with softer employment data and subdued growth, markets began pricing in a potential 25 basis point rate cut at the next RBA meeting.

Meanwhile, the US dollar experienced choppy trading. Hawkish Fed commentary lifted the greenback early in the week. However, disappointing jobs data quickly reversed those gains. The non-farm payrolls report missed expectations, and wage growth slowed. Traders now see a 95% chance of a Fed rate cut in September, up from 50% the day before. You can review the official Fed meeting calendar here.

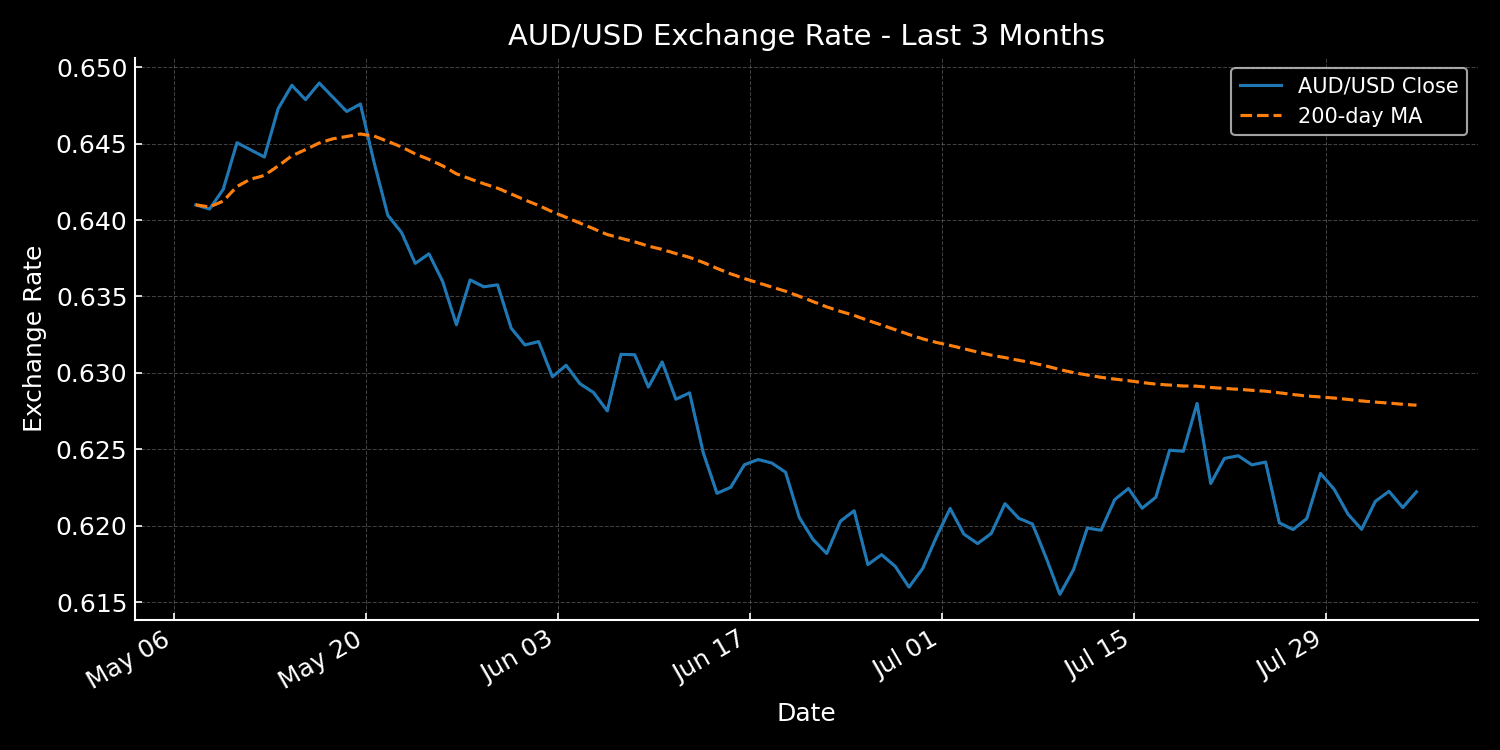

AUD/USD fell to 0.6415 but later rebounded above 0.6460. Traders are now watching for clearer central bank signals to drive the next move. With limited economic data this week, the pair could remain in a tight range unless new headlines emerge.

Source: Yahoo Finance | Chart style: Dark Mode | Data range: Last 3 months

Technically, AUD/USD is holding within an upward-sloping flag, in place since April. While this pattern suggests bullish potential, buyers lack momentum. The 200-day moving average at 0.6390 is nearby support. Resistance sits between 0.6630 and 0.6640, where rallies have stalled in recent months.

In the short term, AUD/USD may continue a slow grind higher. However, sentiment could shift quickly with any surprise from central banks or macro data. Traders should remain alert to new developments and policy rhetoric.

With sentiment fragile and key data ahead, AUD/USD pressured remains a likely theme in the short term. Market positioning will depend on how rate expectations evolve on both sides of the Pacific.