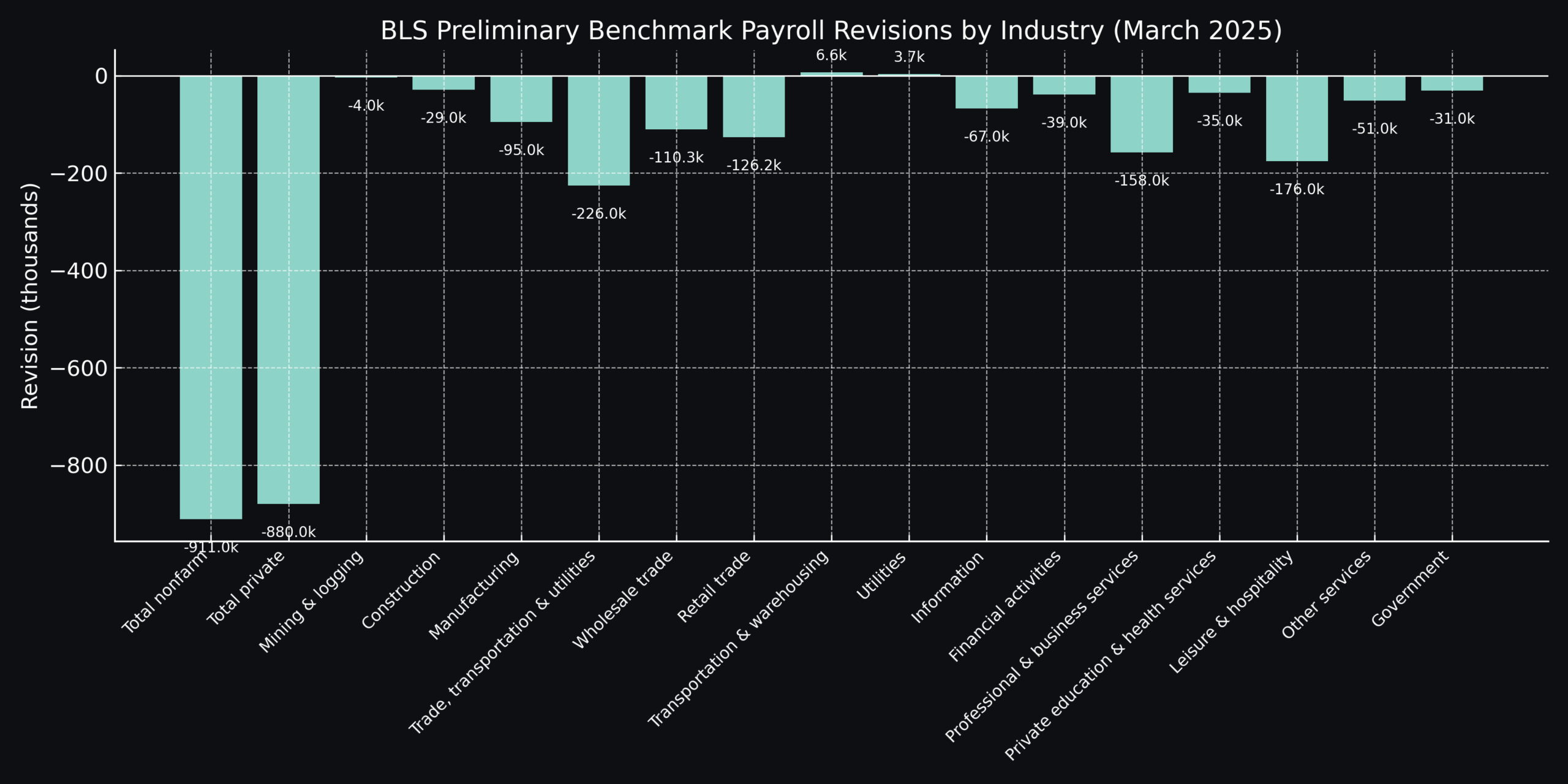

Markets price in expectations, not certainties. When large revisions to employment data are published or when consumer-price readings diverge from forecasts, that information changes the way investors allocate across bonds, equities, currencies and commodities. Payroll revisions adjust the historical baseline for the labour market; CPI prints inform the prospective path for monetary policy. Both inputs feed directly into expectations for rates, risk premia and portfolio positioning. For more detail, see the Bureau of Labor Statistics payroll data and the Federal Reserve’s monetary policy updates.

Asset class reactions to payroll revisions and CPI data

Bonds. Fixed income tends to react first to changes in perceived policy trajectory. Weaker labour data or softer inflation typically lowers short-term rate expectations and can flatten or steepen curves depending on the balance between growth and inflation signals. Sovereign spreads can also reprice on political or fiscal concerns that affect perceived credit risk.

Equities. Equities are sensitive to both growth momentum and financing costs. Softer data that increases the probability of policy easing can be supportive for risk assets, particularly when earnings remain resilient. Conversely, a surprise rise in inflation can tighten financial conditions and weigh on higher-multiple sectors.

Currencies. FX reflects relative policy and macro strength. A move that reduces the expected path of one central bank versus another typically drives currency flows accordingly — the more dovish the path, the greater the downside pressure on that currency, all else equal.

Commodities. Inflation-sensitive commodities such as gold and energy often react to both real rate expectations and safe-haven demand. Gold can rally on rising uncertainty or on expectations of lower real yields. A global overview of inflation and commodity moves is available via Trading Economics CPI data.

Interpreting payroll revisions alongside inflation data

- Magnitude vs. trend: One-off revisions are less informative than persistent directional changes to employment or inflation.

- Policy implications: Ask how the print changes the central bank’s expected path — does it make easing more or less likely?

- Cross-market confirmation: Look for corroborating signals across yields, credit spreads, and FX rather than relying on a single data point.

Positioning strategies around payroll and CPI events

For investors and risk managers, the prudent response is to align exposure to a coherent view of policy risk and growth momentum. That may mean reducing duration when inflation surprises to the upside, or favouring cyclical equity exposure when labour and activity indicators soften and policy loosens. Hedging conditional on scenarios — rather than betting on a single outcome — helps manage the inevitable uncertainty around data revisions and milestone inflation releases.

Key takeaways on payroll revisions and CPI impact

- Payroll revisions change the baseline for employment but must be judged alongside trend metrics.

- CPI prints remain a primary input for rate expectations; the reaction depends on whether core or headline components surprise.

- Look across bonds, equities, FX and commodities for confirmation before changing convictions.

- Scenario-based risk management is more effective than trying to time a single data-driven move.

By keeping focus on how new information alters the policy and growth outlook — rather than on headlines in isolation — market participants can respond in a measured, impartial way that emphasises process over prediction.