Policymakers and investors often focus on the “dual mandate” of price stability and maximum employment. However, the mandate market risk is becoming more relevant. The Federal Reserve Act also instructs the Fed to promote “moderate long-term interest rates.” This little-known goal could influence future policy and create risks for investors if long yields stay elevated while the Fed cuts short-term rates.

Fed Third Mandate Market Risk: What the Statute Says

The Federal Reserve Act sets three objectives: maximum employment, stable prices, and moderate long-term interest rates. The third goal is often ignored in financial commentary, but it remains legally binding. If long yields rise sharply while inflation falls and growth slows, pressure could mount for the Fed to act.

Why the Fed Third Mandate Matters for Investors

When policy rates are cut but long-term yields stay high, a policy gap opens. Rate cuts support the labor market and short-term growth. But higher long yields mean mortgage rates and corporate borrowing costs remain elevated. This also increases the government’s interest expense. Political leaders could demand stronger Fed action to push yields down, potentially using tools beyond rate cuts.

Policy Tools That Could Be Used

The Fed could halt balance-sheet runoff to add demand for Treasuries. It might even restart asset purchases targeting longer maturities. In a more extreme scenario, yield curve control could be introduced, setting an explicit cap on yields. These moves would be significant and could impact market expectations for years.

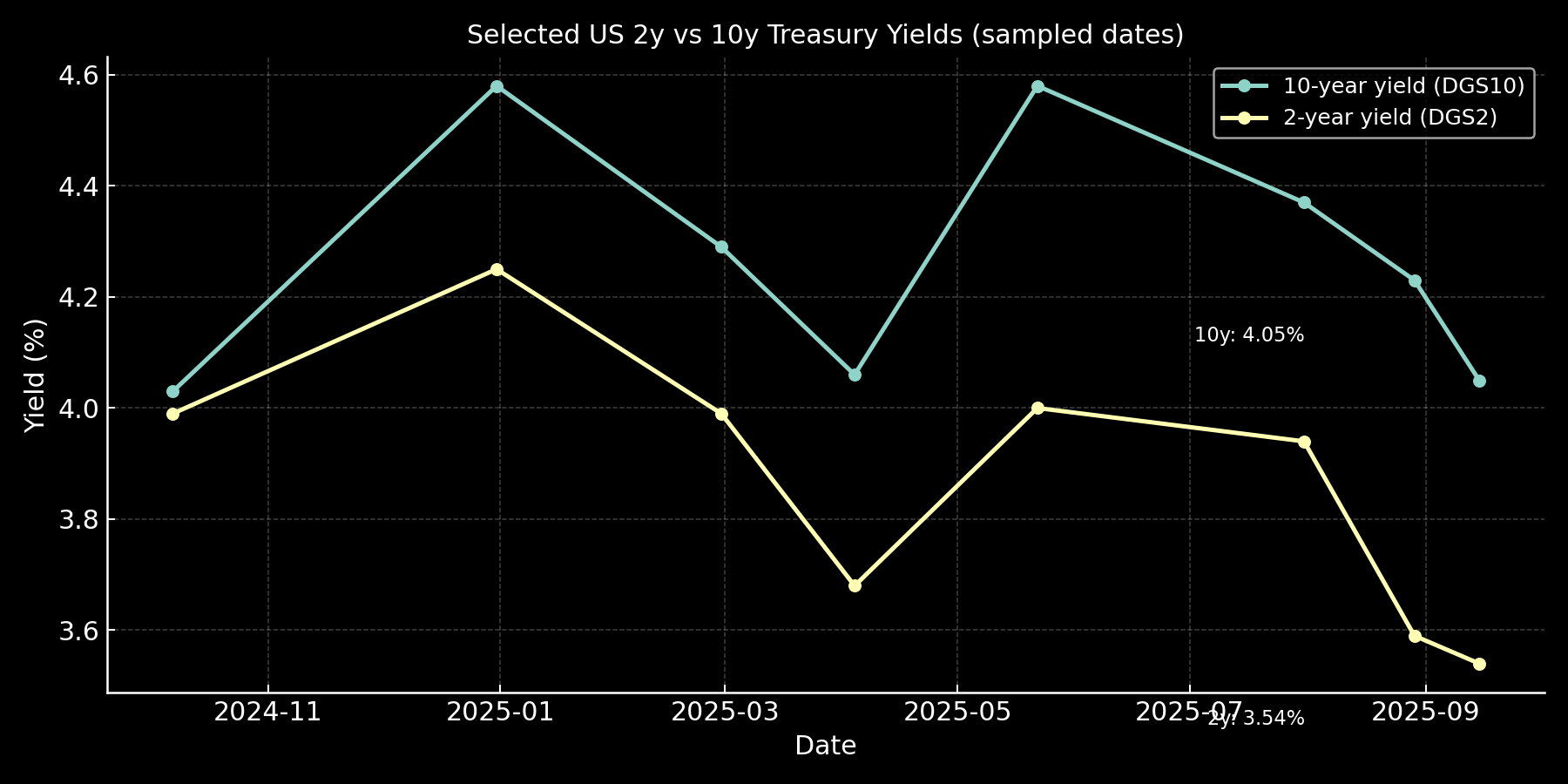

Figure: Sampled US 2-year vs 10-year Treasury yields (dark mode). Data: FRED (DGS10, DGS2).

Source: Federal Reserve Bank of St. Louis (FRED), DGS10 & DGS2. Chart by author.

Political and Market Context

Recent Fed appointments and public testimony have highlighted all three statutory goals. Some officials have quoted the full mandate in Senate hearings, signaling it could guide future decisions. External pressure from Treasury officials or the White House could accelerate a pivot toward long-end rate management.

Investor Takeaways

Investors should prepare for a range of outcomes. If the Fed takes steps to lower long-end yields, duration trades could rally. If inflation expectations rise and the Fed resists direct intervention, the curve could steepen sharply. Reviewing duration exposure, hedges, and liquidity in long bonds may help manage this evolving risk.

Further Reading

For the full statutory text and policy framework, see the Fed’s monetary policy goals page. For recent developments on Fed appointments and Treasury commentary, see Reuters coverage of Fed confirmations and Treasury commentary.