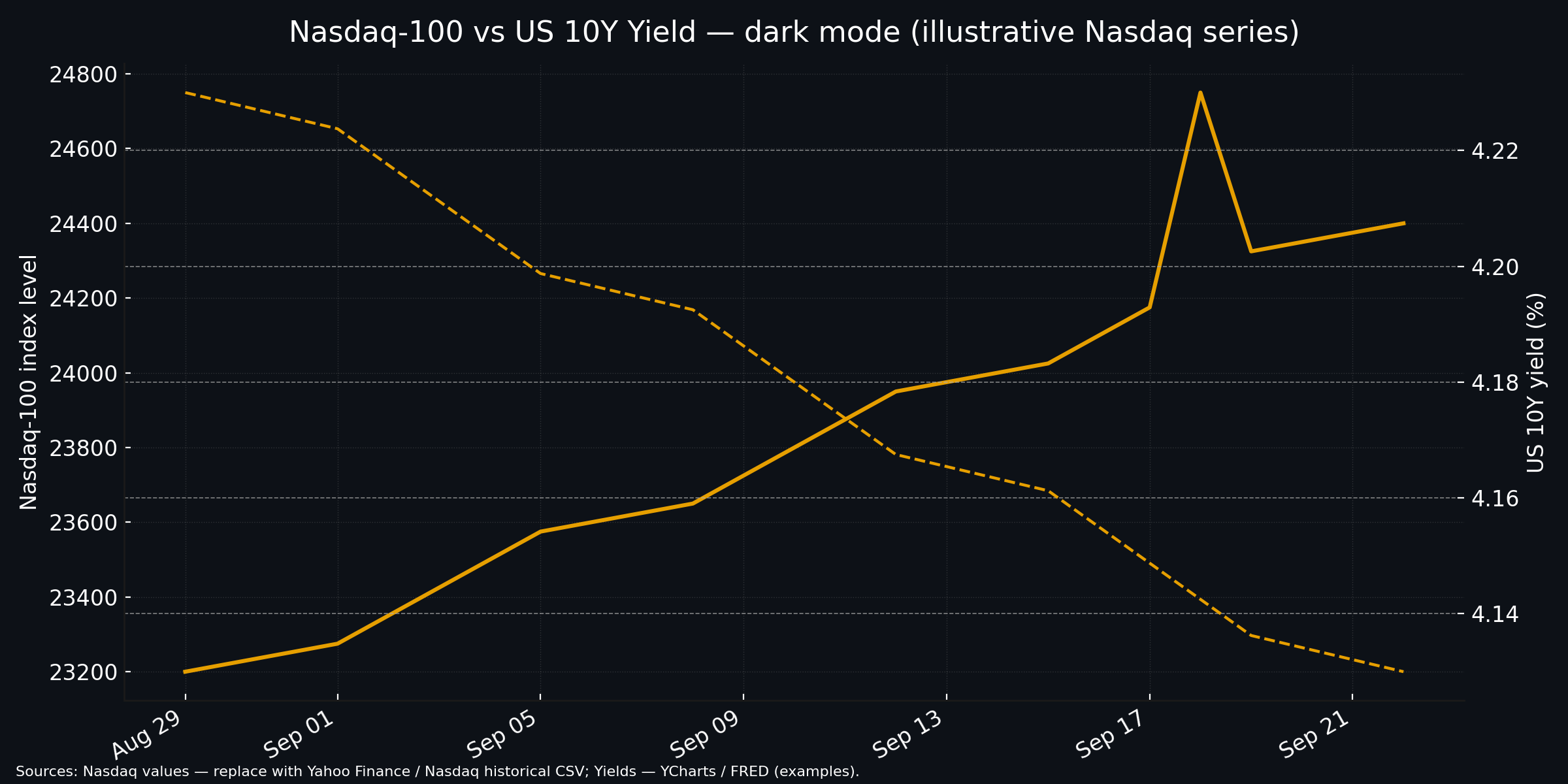

Nasdaq Strength remained evident as investors digested two powerful narratives: a major industry partnership in semiconductors and a shift in U.S. monetary policy. The semiconductor news re-ignited cyclical technology names while the central bank’s decision to reduce rates lowered the hurdle for long-duration growth stocks. Together they widened the market’s participation beyond headline mega-caps.

Deal dynamics: why the chip news mattered

A technology partnership between two major chip companies altered the outlook for product roadmaps, integration of CPU and GPU platforms, and potential PC and data-centre refresh cycles. The announcement reassured some investors that AI-related capital expenditure remains an active driver of demand and that platform alliances can accelerate time-to-market for new, monetizable hardware designs. Market reactions were visible across chip suppliers, systems vendors and software infrastructure providers as traders re-priced future revenue potential.

That single corporate development changed the risk calculus for several technology suppliers: it reduced some supply-chain concentration concerns and highlighted new routes to commercialising AI workloads in both servers and end-user devices. The news also prompted a re-assessment of sector winners and losers as investors looked for firms that will benefit from expanded CPU+GPU architectures and refreshed PC demand.

Policy backdrop: lower rates and market multiples

On the macro side, the Federal Open Market Committee trimmed its policy rate and signalled a willingness to consider further easing. Lower expected policy rates ease financing costs, raise the present value of future cash flows and often support higher multiples for growth companies — particularly those with earnings expected further out. At the same time, signs of cooling in the labour market helped reduce fears that persistent wage pressure would force a return to restrictive policy. This macro shift has been a significant tailwind for Nasdaq Strength, encouraging risk-taking in growth-heavy sectors.

Breadth and the sustainability question

Importantly, the recent advance showed signs of broader participation: small- and mid-cap groups and cyclical pockets joined the rally rather than leaving all the gains to mega-cap technology names. Improved breadth reduces the tail risk associated with overly concentrated rallies, though investors remain attentive to the next round of earnings, order flows and whether AI headline activity converts into durable bookings and margin expansion.

Sources: Yahoo Finance (NDX historical),

YCharts (10Y yield),

FRED (DGS10).

Near-term watchlist

- Corporate execution: product launches, order momentum and guidance from hardware suppliers.

- Rates and yields: whether bond markets hold lower yields or re-price tighter on growth surprises.

- Market breadth: continued participation across sectors will be a key signal of durability.

For investors, the current environment favours disciplined positioning: acknowledge the upside created by easier policy and industry partnerships, but balance that with careful attention to valuations, earnings delivery and macro data that can quickly reframe expectations.

Relevant official and primary sources:

Federal Reserve statement,

company announcement, and

market coverage.