US jobs data has triggered strong market reactions, with investors betting the Federal Reserve may deliver a larger rate cut at its next meeting. The latest non-farm payrolls report showed weaker hiring, raising questions about the health of the labour market and the pace of economic growth.

Non-farm payrolls increased by only 22,000, far below forecasts. The unemployment rate rose to 4.3%. Revisions also lowered job gains in previous months, adding to concerns about slowing momentum. Traders had already expected a 25 basis point cut, but now many see a 50 basis point move as possible.

Investors now wait for the next inflation release. Analysts expect price pressures to stay sticky but not high enough to derail the case for rate cuts. A hotter number could spark short-term volatility, yet markets still see the Fed leaning toward easier policy in the months ahead.

Global stocks trade close to record highs. Investors keep buying technology and growth stocks while reducing exposure to cyclical sectors. The US dollar weakened as yields dropped, reinforcing the shift in positioning across markets.

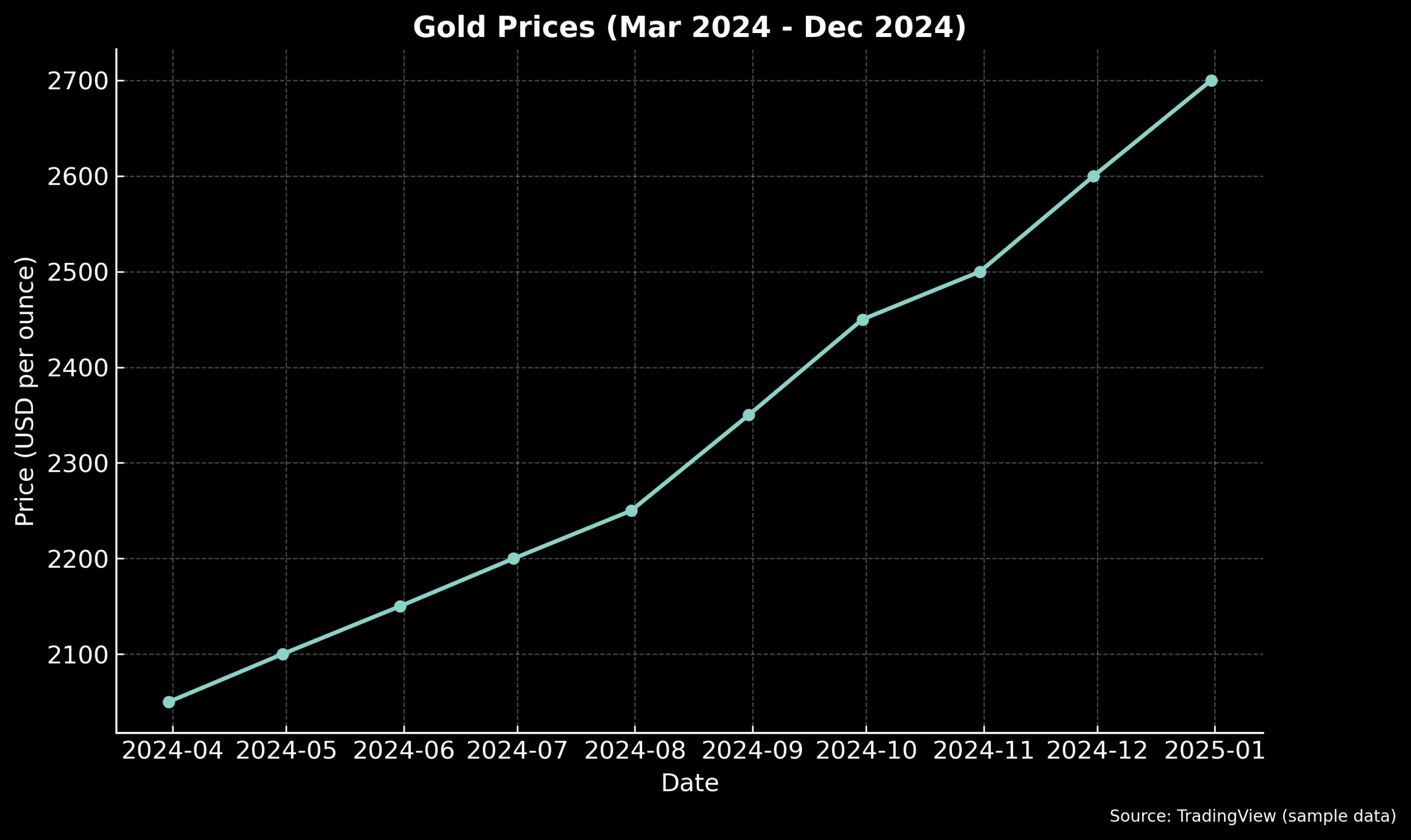

Gold leads the rally. Prices hit new records, with $3,600 per ounce viewed as the next psychological level. Falling yields, a softer dollar, and central bank diversification continue to drive demand. Traders see $3,500 as support if prices pull back.

Oil tells a different story. Prices fell as weaker US demand and signals of a possible OPEC supply boost in October weighed on crude. Softer demand combined with supply risks leaves the energy market vulnerable to further declines.

Overall, the latest US jobs report increased pressure on the Fed. Markets now debate whether the central bank will cut rates by 25 or 50 basis points. Gold and equities show the clearest response to the prospect of easier policy. For more detail on market moves, visit TradingView.