Fed Cuts and BoE decisions have dominated the latest central bank headlines. The Federal Reserve delivered a 25 basis-point rate cut. Meanwhile, the Bank of England held rates steady at 4%. Both moves came with updated guidance and projections. Markets now have plenty to digest as they reassess the path for global monetary policy.

The Fed’s projections showed a modest easing trajectory. However, the distribution of policymakers’ rate forecasts (the “dot plot”) was wide. This created uncertainty about the timing and scale of additional cuts. A single dissent favored a larger 50 bp move, highlighting divisions within the committee. These factors contributed to a perception of a lower-conviction Fed. As a result, major asset classes reacted in a mixed and sometimes contradictory way.

Fed Cuts and BoE: Why Markets Reacted Volatilely

At first, markets welcomed the Fed cut. Equities and gold spiked to test record highs. The dollar and Treasury yields fell. These moves were quickly reversed as investors digested Chair Powell’s remarks and the details of the Summary of Economic Projections. The projections suggested a slower, data-driven approach to policy easing. The “trough rate” implied by the Fed remains above market expectations. This dampened the most aggressive easing bets.

Bank of England: a cautious tilt

The Bank of England kept Bank Rate unchanged. It also announced a slower pace of quantitative tightening, reducing gilt runoff to £70bn over the next year. Markets read this as “less hawkish than feared.” The move supported gilts and softened sterling slightly. The 7–2 vote split shows the MPC remains divided, but overall guidance stays cautious and data dependent.

Visual Comparison:

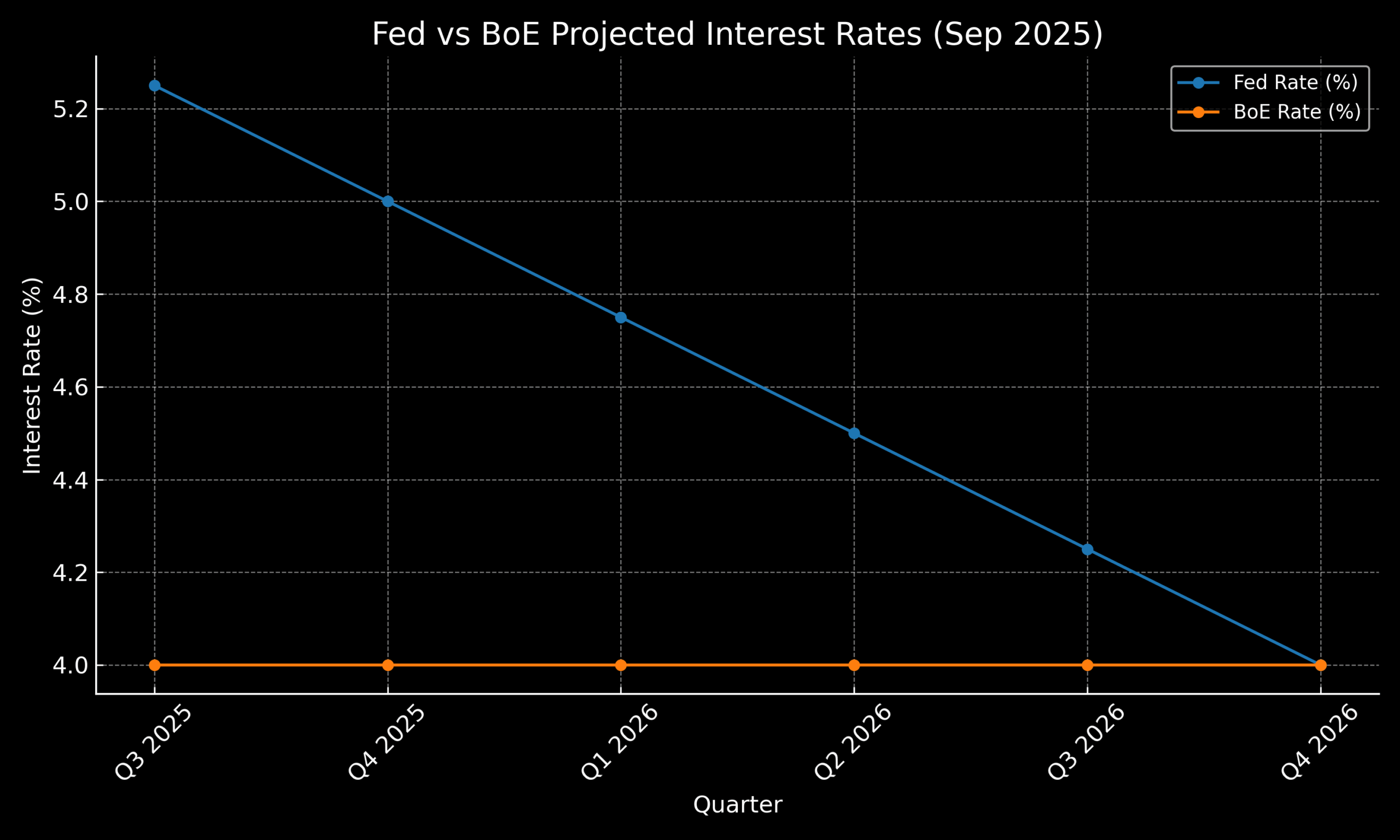

The graph above shows the projected interest rate paths for both the Federal Reserve and the Bank of England as of September 2025. While the Fed has initiated rate cuts, the BoE has maintained its rate, reflecting different policy directions.

What to watch next

Labour market trends and core inflation releases will drive policy expectations in the coming months. A sharp rise in unemployment could push the Fed toward further easing. Conversely, sticky inflation may justify keeping rates higher for longer. For the BoE, continued progress on disinflation would allow policy to remain on hold. Any unexpected uptick in inflation could reignite debate about the need for more restraint.

For investors, this environment calls for flexibility. Rate expectations can shift rapidly as new data arrives, keeping volatility elevated. Short-end futures, OIS pricing, and upcoming core PCE data will be critical signposts for the path ahead.

Primary sources and further reading: Federal Reserve — FOMC statement and projections, Bank of England — Monetary Policy Summary (Sept 2025).