Wall Street ended last week with modest gains as traders balanced rotation out of high-growth technology stocks with renewed interest in cyclical and value names. While the Dow Jones stood out on relative strength, the Nasdaq 100 and S&P 500 showed signs of fatigue as stretched valuations and mixed earnings weighed on sentiment. The upcoming Jackson Hole Symposium is now in focus as markets look for guidance on the Federal Reserve’s next steps.

Macro drivers to watch on Wall Street

Investors are weighing a softer University of Michigan consumer sentiment reading against stronger-than-expected retail sales data. The combination leaves growth expectations intact, but inflation concerns linger. With the Federal Reserve still emphasising data dependence, Chair Powell’s remarks in Wyoming could recalibrate market probabilities for a September policy move.

Rotation and positioning

Flows show an increasing tilt towards domestic cyclicals and small caps, while defensives remain steady. Technology leaders remain more vulnerable to earnings revisions and guidance updates, especially in semiconductors where order visibility is clouded by export restrictions. Despite this, the long-term structural AI story remains supportive of valuations, keeping the group a central driver of equity sentiment.

Earnings season—final stretch

Retail heavyweights reporting this week will give a fresh look at discretionary spending patterns, inventory health, and margin pressures. Traders will closely follow traffic versus ticket size and back-to-school trends. Later, a major AI platform company’s earnings could set the tone for semiconductors and broader tech performance into month-end. For a wider view of earnings season updates, see Reuters Markets.

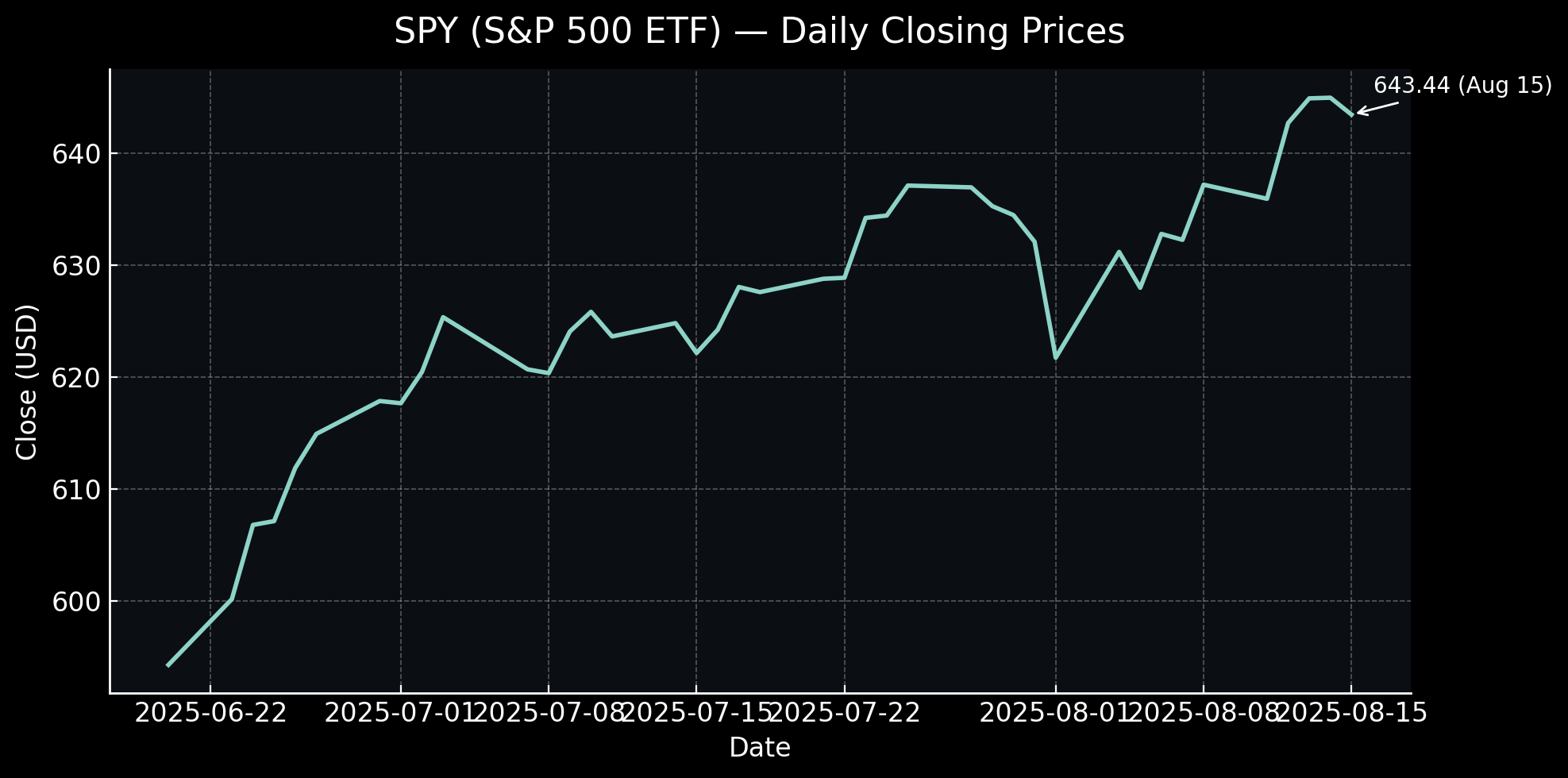

Technical picture

US Tech 100: The uptrend from late spring remains intact, but momentum indicators like RSI show divergence, signalling caution near resistance. A break above recent highs would reopen the trend continuation case, while a dip below the rising moving-average band could trigger a corrective phase back to earlier support zones.

US 500: Overhead supply remains a challenge near recent peaks. Sustained support at short-term levels is essential; failure could prompt a retest of the July pivot, while higher lows keep the bullish structure in place.

Key factors for the week ahead

- Policy: Jackson Hole remarks on inflation and growth risks.

- Retail earnings: Updates from leading US retailers on consumer trends.

- Technology: Semiconductor guidance on demand, exports, and supply chains.

- Economic data: Consumer and labor figures that shift Fed expectations.

Bottom line for Wall Street

Wall Street maintains a constructive bias as breadth improves, but caution is warranted with multiple catalysts clustered in the days ahead. Indices can grind higher if policy risks remain contained, while stock pickers should stay selective, favouring names with solid guidance and cash-flow discipline.

Past performance is not a reliable indicator of future results. This content is general in nature and does not constitute financial advice.