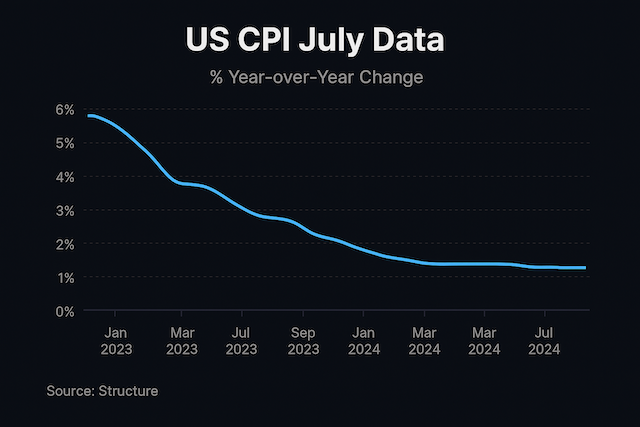

The US CPI July data reveals a mixed inflation picture, complicating expectations for the Federal Reserve’s upcoming policy decisions. Headline CPI remained at 2.7% year-over-year, matching June and slightly below forecasts of 2.8%. Month-on-month, the index rose 0.2%, down from June’s 0.3% increase.

Core CPI, excluding food and energy, increased 0.3% for July, marking the largest monthly gain since January. The year-over-year core reading rose to 3.1%, higher than expected, indicating that underlying price pressures remain persistent. Tariff-sensitive categories, including furniture, apparel, and certain food items, contributed notably to this increase. Housing and transportation costs also played a role in supporting core inflation levels.

Despite higher core inflation, market expectations for a September Fed rate cut remain strong. Slower headline growth and broader disinflationary trends have maintained optimism for looser monetary policy. Traders are analyzing both headline and core figures, creating mixed signals for equities and currencies. The US CPI July data is being closely watched for signs of whether inflation is truly easing or if underlying pressures could persist into the coming months.

Equities reacted positively, with the S&P 500 continuing its upward momentum and closing near recent highs. The combination of stable headline inflation and anticipated monetary easing has bolstered investor confidence. For detailed S&P 500 data, see Investing.com. Some analysts note that sectors like technology and consumer discretionary are likely to benefit if the Fed maintains a dovish approach.

The US dollar softened slightly after the CPI release, reflecting market belief that the Fed may remain accommodative despite stronger core inflation. This divergence between headline and core readings underscores the challenges policymakers face in interpreting inflation dynamics. Currency markets remain sensitive to any future signals from the Fed regarding interest rates and inflation outlooks.

July’s CPI data emphasizes the complex nature of current inflation trends. While headline prices show moderation, persistent core inflation indicates underlying pressures have not fully eased. Investors and traders will closely monitor upcoming economic reports, including retail sales, employment data, and manufacturing indicators, to gauge the Fed’s potential moves.

Overall, markets are adjusting portfolios based on these mixed CPI signals. The interplay between headline moderation and core strength will continue to influence market sentiment, Fed policy expectations, and positioning in both equities and currency markets in the near term.